Worldwide Jet Engine Warranty Expenses:

In 2023, the top global jet engine OEMs paid $1.58 billion in warranty claims, set aside $1.88 billion in warranty accruals, and held a collective $4.88 billion in warranty reserves. The industry average claims rate was 1.29%, and the average accrual rate was 1.53%.

Last week, we took a look at five years of "Worldwide Aviation Warranty Expenses." This week, we're analyzing the warranty expenses of their counterparts in the global aviation sector, the jet engine manufacturers.

In 2020, the major airframe OEMs saw revenue decrease significantly, and lowered their warranty accruals as a result, but claims kept coming in at the same rate, despite the drop in sales. We'll see the same story from the jet engine OEMs.

To compile this report, first we identified the world's top jet engine manufacturers, and then gathered data on their warranty expenses from their annual reports. We measured three key warranty metrics: the amount of claims paid the amount of accruals made, and the end-balance of the warranty reserve fund.

In addition, we gathered data on each airframe OEM's product sales revenue, which we used to calculate two additional warranty expense rates: claims as a percentage of sales (the claims rate), and accruals as a percentage of sales (the accrual rate).

Since the global aircraft engine OEMs report in U.S. dollars, Euro, and British pounds, we converted all data to U.S. dollars using the Internal Revenue Service's Yearly Average Currency Exchange Rates table in order to create the following charts.

Worldwide Jet Engine Industry

The global jet engine industry includes several large manufacturers, and many additional joint ventures between many of the aviation sector's top players. And as with the airframe manufacturers, some of the top jet engine OEMs are also defense contractors, and civilian aircraft sales are only a portion of their business.

However, military contracts typically do not come with traditional product warranties attached. Instead, they come with a unique type of military service contract. As such, we do not factor revenue generated from defense contracts into the segmented product sales revenue figures. In other words, we don't factor revenue generated from military contracts into the denominator of the formula used to calculate the warranty expense rates, because we know that repair costs generated by those products are not considered warranty costs in financial statements.

Among the "pure play" jet engine OEMs, we have Rolls-Royce Holdings plc, based in the United Kingdom. Rolls-Royce is not to be confused with Rolls-Royce Motor Cars, which has been a subsidiary of BMW since 2003.

There's also the Germany-based MTU Aero Engines AG, which was initially formed as a joint venture between MAN Turbo and Daimler-Benz back in 1968. However, the company traces its origins back to when BMW spun-off its aircraft engine division in 1934, and still uses the same plant in Allach, near Munich. MTU became an independent company through a sale to a private equity firm, which then listed all of MTU's shares on the stock exchange.

U.S.-based Williams International is also a jet engine pure-play, but does not report its financial data since it is privately owned.

And newly, there's GE Aerospace, a pure-play in the aircraft engine industry since April 2024, after General Electric divested its healthcare (GE HealthCare) and energy (GE Vernova) divisions. HealthCare was spun off in January 2023, but the split between GE Aerospace and Vernova is so new that our five-year data frame only includes data from General Electric Co.

In fact, most of the top jet engine manufacturers are conglomerates also engaged in sectors including defense, security, and communications.

There's Safran Aircraft Engines, formerly known as Snecma, a division of the France-based aerospace and defense corporation Safran SA; Honeywell Aerospace, a division of Honeywell International Inc.; and Pratt & Whitney, a subsidiary of RTX Corp., formerly known as Raytheon Technologies Corp. RTX Corp. has owned Pratt & Whitney since the 2020 merger of Raytheon Co. and United Technologies Corp.

And then there's many more jet engine joint ventures amongst the top aerospace industry players.

In the United States, The Engine Alliance is a 50/50 joint venture between GE Aerospace and Pratt & Whitney. And cross-Atlantic, CFM International is a 50/50 joint venture between GE Aerospace and Safran Aircraft Engines.

Boeing and Safran also have a 50/50 joint venture to design, build, and service auxiliary power units.

There's also PowerJet, a 50/50 joint venture between Safran Aircraft Engines and the Russian aircraft engine manufacturer NPO Saturn, a division of United Engine Corporation, which in turn is owned by the Russian state-owned defense conglomerate Rostec. As one might expect, France's sanctions against Russia following the 2022 invasion of Ukraine have led to PowerJet terminating service for its engines, including parts, technical support, engine maintenance, and repair services.

And notably, there's International Aero Engines (IAE) AG, formed in 1983 as an engine consortium consisting of Pratt & Whitney, Rolls-Royce, MTU Aero Engines, Italy-based Fiat Avio, and the Japanese Aero Engine Corporation (JAEC). After Fiat Avio and Rolls-Royce exited the consortium (though both remain parts suppliers), IAE is now 50% owned by Pratt & Whitney, 25% owned by MTU, and 25% owned by JAEC.

The former Fiat Avio was sold by the Fiat Group in 2003, to a consortium 70% owned by the American private equity firm The Carlyle Group, and 30% owned by the Italian Finmeccanica S.p.A., now known as Leonardo S.p.A. The Carlyle Group later sold its portion of Avio S.p.A. to the British private equity firm Cinven Limited. The company was then split in two, with Avio's aviation division spun-off and acquired by General Electric 2012, while Avio's space division retains the Avio S.p.A. name, and continues to be jointly owned by Cinven and Leonardo, collaborating with the European Space Agency.

ITP (Industria de Turbo Propulsores) Aero was formed in 1989 as a joint venture between Spanish conglomerate SENER and Rolls-Royce. And in turn, it belongs to the Europrop International (EPI) GmbH consortium, which was founded in 2002, and consists of MTU Aero Engines, Safran Aircraft Engines, Rolls-Royce, and ITP Aero.

There's also EuroJet Turbo GmbH, which is a consortium founded in 1986, which consists of Rolls-Royce, MTU, ITP, and Avio.

Of course, there's also more jet engine, defense contractor, joint venture, and consortium counterparts of these manufacturers in Russia and China, as we indicated with our mention of Rostec's previous collaboration with Safran. However, as one would expect, there's no publicly available warranty data for these companies.

In the following charts, we present data from GE, RTX, Safran, Rolls-Royce, Honeywell, and MTU. These six represent almost all of the warranty expenses of the worldwide civil aircraft engine industry, and all six luckily publish their warranty expenses in their annual reports.

Warranty Claims Totals

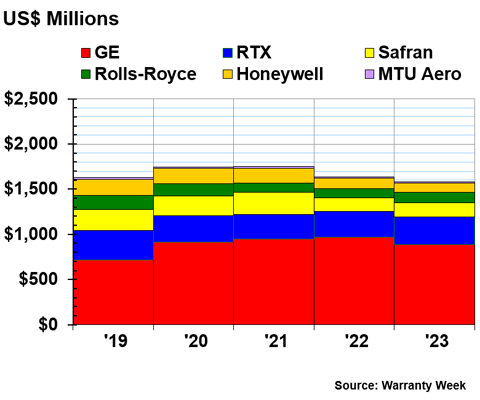

In Figure 1, we'll take a look at the total annual product warranty claims payments made by each of the jet engine OEMs, from 2019 to 2023.

Figure 1

Top Jet Engine Makers Worldwide

Claims Paid per Year

(in millions of U.S. dollars, 2019-2023)

In 2023, the six top jet engine manufacturers paid a total of $1.58 billion in warranty claims, a -3% decrease from 2022.

In 2023, GE paid $886 million in warranty claims, a decrease of -8% from the year prior. Fellow American manufacturer RTX paid $308 million in claims in 2023, an increase of 8% from 2022. And Honeywell paid $106 million, a -8% decrease.

Over in Europe, Safran paid $157 million in 2023, a 4% increase from the year prior. Rolls-Royce paid $113 million, a 6% increase. And MTU Aero paid $12 million, a -19% decrease.

Notice that just as we saw with the global airframe manufacturers, the jet engine manufacturers saw no interruption to warranty claims during the 2020 pandemic, despite the interruptions to global air travel, aircraft sales, and, as we'll see in Figure 2, warranty accruals.

Warranty Accrual Totals

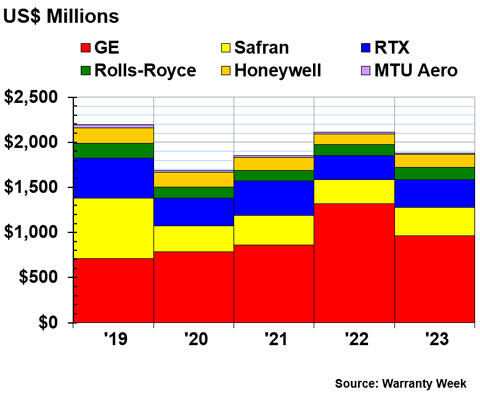

Figure 2 shows the total warranty accruals made by the six top jet engine OEMs, from 2019 to 2023.

Figure 2

Top Jet Engine Makers Worldwide

Accruals Made per Year

(in millions of U.S. dollars, 2019-2023)

In 2023, the jet engine manufacturers set aside a total of $1.88 billion in warranty accruals, a -11% decrease from 2022.

GE accrued $961 million, a -27% decrease from 2022. It's likely that the higher accruals in 2022, and the drop in 2023, are associated with GE Vernova's wind turbines, rather than GE Aerospace's jet engines. Now that the two have separated, data released in the future will help us determine the ratio of warranty expenses between the two GE divisions.

In 2023, Safran accrued $319 million, a 19% increase from 2022. RTX accrued $305 million, up 16%. Rolls-Royce accrued $139 million, up 15%. Honeywell accrued $139 in 2023, an increase of 19%. And MTU Aero accrued $12 million in 2023, a decrease of -40% from the year prior.

Warranty Expense Rates

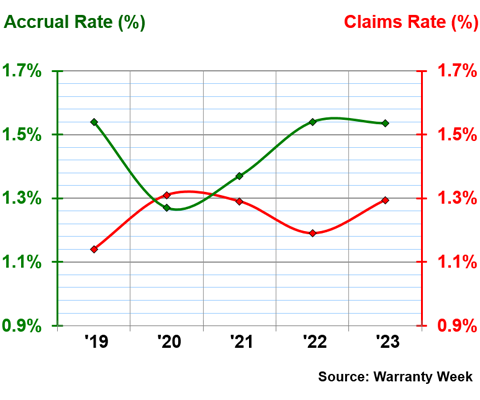

Figure 3 shows the jet engine industry-wide average warranty claims and accrual rates over the five-year period.

Figure 3

Top Jet Engine Makers Worldwide

Average Claims & Accrual Rates

(as a % of product sales, 2019-2023)

In 2023, the top global jet engine manufacturers had an average warranty claims rate of 1.29%, and an average warranty accrual rate of 1.53%.

In 2023, GE had a claims rate of 3.31%, at the highest end of the spectrum. Next was MTU Aero, with a claims rate of 1.55%, followed by Safran, with a claims rate of 1.51%. Notably, Safran's claims rate doubled from 2022 to 2023.

Below the industry average, Rolls-Royce had a claims rate of 1.27% in 2023, followed by RTX, with a claims rate of 0.62%. And with the lowest claims rate of the bunch was Honeywell, which paid an average of 0.41% of its product sales revenue in warranty claims during 2023.

GE also had the highest accrual rate of the bunch, at 3.59% in 2023.

Safran's accrual rate also doubled from 2022 to 2023, along with its claims rate. In 2023, Safran had an accrual rate of 3.07%.

Rolls-Royce had a claims rate of 1.57% in 2023, and MTU Aero had a claims rate of 1.55%.

Below the industry average, RTX had an accrual rate of 0.62% in 2023, and Honeywell had an accrual rate of 0.54%.

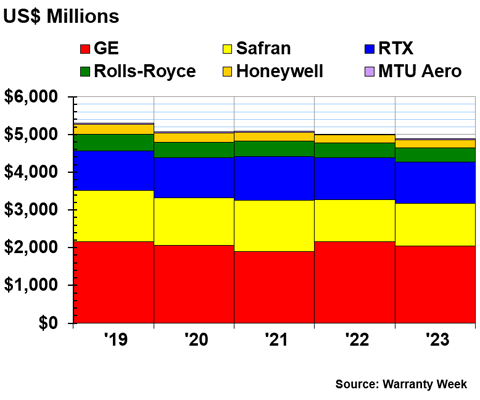

Warranty Reserve Balances

Our final warranty metric is the year-end-balance of each manufacturer's warranty reserve fund. Figure 4 shows reserve end-balances for the top six global jet engine OEMs, from 2019 to 2023.

Figure 4

Top Jet Engine Makers Worldwide

Reserves Held per Year

(in millions of U.S. dollars, 2019-2023)

At the end of 2023, the global jet engine industry held a collective $4.89 billion in warranty reserves, a -3% decrease from the end of 2022.

GE had the largest reserve fund of the group, with $2.05 billion in the fund at the end of 2023, a -5% decrease from the end of 2022.

Safran had the next-largest warranty reserve fund, with $1.12 billion at the end of 2023, a minute -0.4% decrease from the end of 2022. RTX held $1.09 billion in reserves at the end of 2023, a -2% decrease from the end of the year prior.

The warranty reserve funds of the remaining three jet engine OEMs are significantly smaller than those of GE, Safran, and RTX, each of which held over $1 billion. Rolls-Royce held $381 million at the end of 2023, a -3% decrease from the end of 2022. Honeywell held $219 million, an increase of 3%. And MTU Aero held just $21 million in warranty reserves at the end of 2023, a 3% increase from the end of the year prior.